Optimism abounds in OBR forecasts, but just how feasible are they?

When former Tory chancellor George Osborne created the Office for Budget Responsibility (OBR) in 2010, he was unlikely to have envisioned it would become the source of financial market turmoil.

But, that upheaval was not the budget watchdog’s fault. Instead, it was former prime minister Liz Truss and ex-Number 11 incumbent Kwasi Kwarteng’s disdain toward the OBR that partly sparked the calamitous response by investors to the pair’s mini budget in late September.

Jeremy Hunt has taken a completely different approach. He made allowing the OBR to mark the government’s fiscal homework a priority.

While the OBR is now one of the UK’s elite economic institutions, its latest set of economic forecasts seem somewhat optimistic.

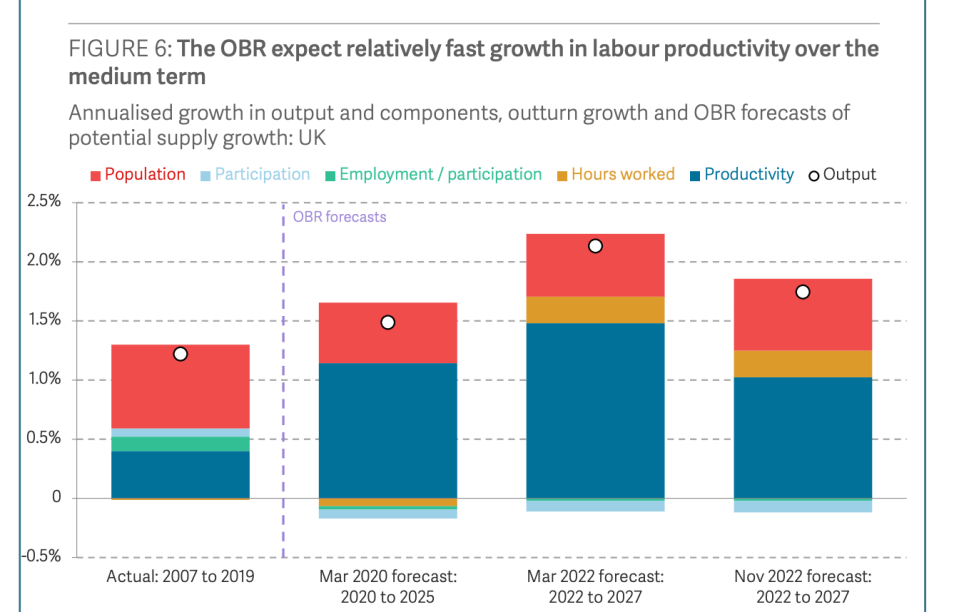

The organisation headed by Richard Hughes, a former senior treasury official, is leaning (very heavily) on assuming UK productivity growth surging over the next five years. It made a similar judgement in its March 2022 forecasts.

In fact, according to consultancy Pantheon Macroeconomics, the budget watchdog thinks long term output per hour growth will hit 1.3 per cent, more than double its average during the 2010s.

The Resolution Foundation estimates that assumption generates a whole percentage point of the OBR’s GDP growth projection over the next five years.

The OBR’s reasoning led it to project the economy will expand more than two per cent each year after 2024, about 0.5 percentage points above the UK’s annual average since the financial crisis in 2008.

As has been well documented, since the global banking system nearly collapsed, Britain has been gripped by a productivity malaise. It has barely inched higher each year.

The productivity estimate “looks too optimistic, given that business investment is set to comprise a smaller share of GDP over the next couple of years than back then,” Samuel Tombs, chief UK economist at Pantheon Macroeconomics, said.

The biggest factor keeping productivity lower has been chronically low business investment.

In fact, in the OBR’s projections, business investment is on track to take a knock from higher interest rates and uncertainty over whether it is worth buying new computers and building new factories during a recession.

The Organisation for Economic Co-operations and Development reckons UK business investment next will grow one per cent, higher than the United States and Germany, but lower than France.

Experts are sceptical about a coming investment boom in the UK.

“The forthcoming recession and higher interest rates suggest we won’t get the private investment growth needed to move the needle for productivity growth. I think it will be hard for the UK to grow consistently at two per cent annual rates across the medium-term,” James Smith, developed markets economist at ING, told City PM

In the autumn statement, Hunt confirmed the 130 per cent investment relief will finish at the end of next March, something the Confederation of British Industry has warned will keep productivity growth tepid.

Stronger population growth will also drive GDP higher, the OBR reckons. Net migration will hover around 215,000 each year over its forecast horizon, increasing the workforce and the economy’s potential output.

Those estimates are up around 75,000 from Osborne’s brain child’s forecasts in March.

That assessment looks more feasible than its productivity bet. Figures from the ONS last week revealed net migration topped 500,000 in the year to June, a record, although the numbers were pushed higher Ukrainians fleeing Putin’s destruction and foreign students who have spent the last two years studying remotely finally moving to the UK.

This influx of foreign workers into the UK labour market is necessary to replace around 900,000 people who left the jobs market since the start of the pandemic.

A large chunk of this group are older workers taking early retirement, suggesting “that many will never return,” the OBR reckons.

According to the OBR, the size of Britain’s workforce will not return to its pre-pandemic trend until around mid 2027, weighing on output. Over the course of the next five years, the labour force will miss out on 0.3 percentage points of growth.

Without an inflow of migrants to replace those workers, Britain will be unable to produce the same volume of goods and services, making the country poorer.

Now, the OBR is not alone in making this next assumption.

For months, economists have been betting households will unleash a wave of savings built up during the Covid-19 crisis when spending opportunities were blocked by lockdowns.

Brits have around £150bn savings above their pre pandemic trend.

The rationale goes as such: “households will… draw on their savings to cushion the impact of higher prices on their consumption,” according to the OBR. In fact, the organisation thinks the savings ratio – the amount of money households set aside each month from their pay packets – could hit zero per cent next year.

Most recent data does not suggest this.

According to the Bank of England, in September, households saved £8.9bn, much higher than previous months. They also spent just £100m on credit cards, compared to £700m in August.

When economic uncertainty rises, people tend to be more cautious. They may avoid taking on more debt for fear of losing their job and being unable to repay lenders. They are more likely to pay off existing debt, particularly when interest rates are rising.

Ultimately, people are highly sensitive to their job security. If they think sometime in the future they could be laid off, then they will save more each month so they can pay for basic necessities should the worst happen.

Exercising greater caution on an individual level makes sense. But, if everyone does it, it sends a chill through the entire economy. That situation seems to be where we are headed. If the savings rate stays elevated, the OBR’s GDP forecasts will come in lower than expected.

Lots of commentators and politicians bashed the OBR in the lead up to the autumn statement earlier this month. Its forecasting record is not great, but it is tough to find any organisaiton which does have a good one.

This is not to say economic forecasts should be binned. Instead, it shows how challenging it is to get them bang on, particularly in a much more uncertain world.

As the old economics saying goes: “It is better to be approximately right than exactly wrong”.